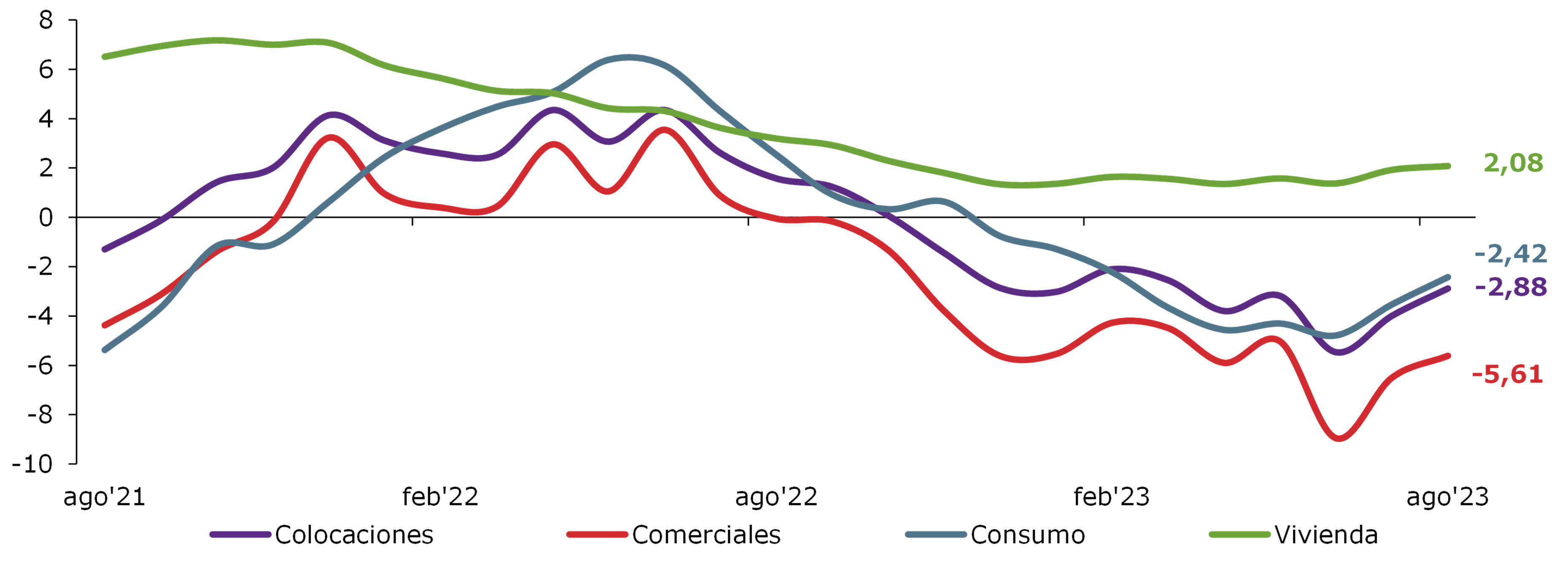

September 29, 2023 - Loans in the banking system fell by 2.88 percent over the past year due to a decline of 5.61 percent in the commercial portfolio (still a lower contraction than the one recorded in July 2023). Consumer loans decreased by 2.42 percent in that span, a figure alleviated by inorganic growth in a banking entity during the month. Housing loans rose by 2.08 percent, better than last month.

Graph 1: Total loans and loans by portfolio in the banking system

(Real annual variation expressed in percentage)

Purple: Total loans. Red: Commercial loans. Blue: Consumer loans. Green: Housing loans.

Regarding credit risk, the loan-loss provisions index and the arrears ratio of 90 days or more declined in August, while the impaired portfolio ratio grew. These stats show dissimilar trends for each portfolio, as shown in commercial loans (decreases in arrears and the loan-loss index) and the housing portfolio (lower arrears and impaired portfolio ratios). Meanwhile, consumer loans recorded a rise in the impaired portfolio ratio, while the loan-loss provisions index showed no variation in consumer and housing operations.

Overall, the loan-loss provisions index fell by 2.53 percent and the arrears ratio of 90 days or more declined by1.94 percent due to lower commercial coefficients and a drop of all indices in the commercial and consumer portfolios. The impaired portfolio ratio was 5.36 percent because of higher coefficients in consumer and housing loans.

Monthly profits for August reached CLP 328,889 million (USD 385 million), a decline of 27.52 percent versus the same month last year. The return on average equity was 16.26 percent and the return on average assets 1.16 percent, both lower than last month and August 2022.

Supervised Cooperatives

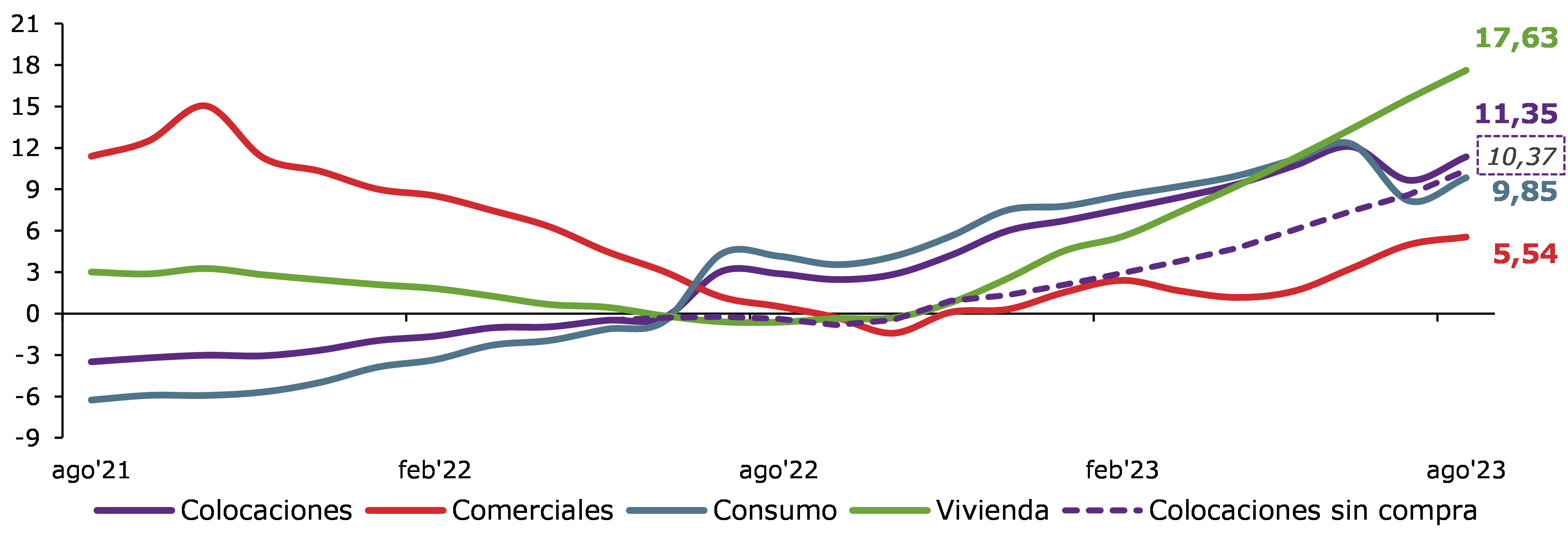

Loans in savings and credit cooperatives supervised by the CMF expanded by 11.35 percent over 12 months. This figure considers the inorganic growth of the consumer portfolio resulting from a portfolio purchase made by a cooperative in 2022, which impacted the industry's activity from the second half of that year onwards. Excluding said effect, loans would have grown by 10.37 percent during August, as Graph 2 shows:

Graph 2: Total loans and loans by portfolio granted by savings and credit cooperatives

(Real annual variation expressed in percentage)

Purple: Total loans. Dotted Purple: Total loans without considering portfolio purchase. Red: Commercial loans. Blue: Consumer loans. Green: Housing loans.

The consumer portfolio, representing 72.01 percent of these loans, is the main reason behind these results after a 9.85-percent growth during the month versus 8.42 percent when not considering the portfolio purchase mentioned earlier. The housing and commercial portfolios increased by 17.63 and 5.54 percent, respectively.

Regarding credit risk, the provisions index declined slightly to 3.69 percent after declines in all portfolios, and the arrears ratio of 90 days or more fell to 2.69 percent after a similar trend in consumer loans. The impaired portfolio ratio was 7.59 percent because of increases in the commercial and housing portfolios. All three indices expanded versus 12 months ago across all portfolios, except for the provisions index and arrears ratio of the housing portfolio.

Monthly profits for August reached CLP 10,994 million (USD 13 million), decreasing by 48.57 percent versus the same month last year. The return on average equity was 11.8 percent and the return on average assets 2.79 percent, both lower than last month and August 2022.

Links to Relevant Documents

- Report on Performance of the Banking System and Cooperatives - August 2023

- Monthly Report on Financial Information of the Banking System - August 2023

- Report on Derivative and Non-Derivative Instruments of the Banking System - August 2023

- Arrears Ratio of 90 Days or More in the Banking System - August 2023

- Report on the Impaired Portfolio of the Banking System - August 2023

- Assets and Liabilities of the Chilean Banking System Abroad - August 2023

- Balance Sheets and Statements of Banks (in plain text format) - August 2023

- Financial Report of Savings and Credit Cooperatives - August 2023